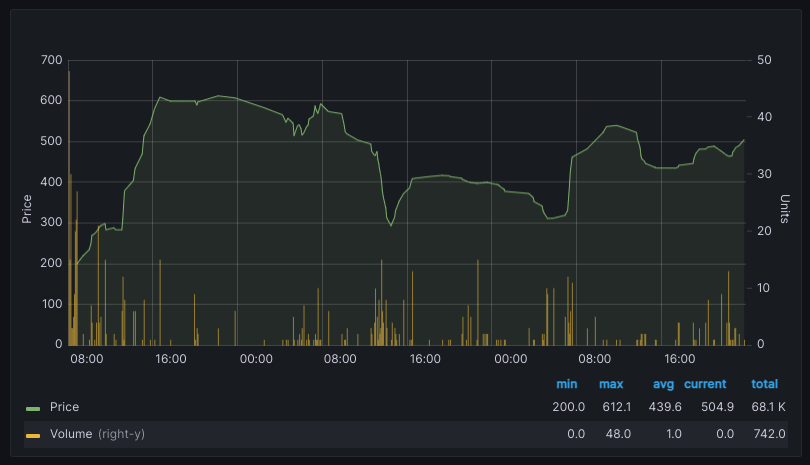

Modeling changes in intraday trading volume is a key component in algorithmic trading strategies. Deep learning can be a useful tool for discovering new edges for investors, but for several reasons the use of recurrent neural network models in financial data have produced mixed results. In this on-going project, I explore the application of deep learning models on time series data by first attempting to replicate on a different data set the methods and results detailed in Libman, et al 2019, which combined Long Short Term Memory (LSTM) networks with support vector regression (SVR) and autoregression (AR).

Blog post coming soon!

|

Github